About the project

Project title: Financial Stability and Improved Policies through Spatio-temporal Hybrid Climate Stress Tests

Flooding is one of Aotearoa New Zealand’s costliest natural hazards, and risk of flooding will increase with climate change to 2100 and beyond. To prepare for this, we need better ways to predicting and understanding the impacts and implications of elevated flooding risk to households, insurers/banks, and the broader economy. We can achieve this with climate stress-testing across geographic space and through time.

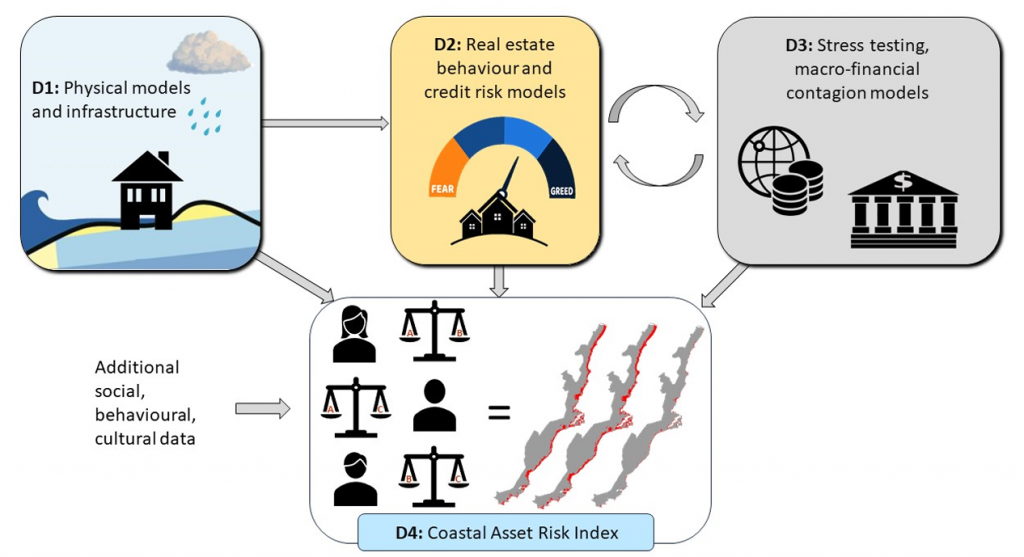

Our SMART Idea is to integrate bottom-up and top-down approaches of stress-testing the resilience of NZ’s real-estate market and financial system to climate-related flooding risks, such that behavioural, macro-economic, and social criteria can be incorporated to expand the range of influences beyond what have previously been considered. this hybridised model will be built upon the foundational blue-skies research in the Marsden funded STRAND project (2021-2024), leveraging and expanding the skilled and highly multidisciplinary research team from five research institutions and numerous research partners (including Reserve Bank of New Zealand and Cotality) and world-leading experts. Specifically, this expanded team will:

1. Improve the physical multi-hazard analysis using site-specific climate and groundwater datasets

2. Factor behavioural responses of market participants (homeowners, banking and insurance firms) and explore how this may affect the pricing of flooding risk

3. Develop better ways to estimate risks to mortgage lending including repayment and defaults

4. Capture the wider effects of flooding risk on the broader economy and financial stability, and

5. Go beyond financial impacts and considers social, physical, and cultural factors with a spatial multi-criteria risk index

Successfully achieving these goals will result in more accurate, applicable, and relevant climate risk estimates that better serve the needs of climate risk pricing and adaptation policies. This will build NZ’s capabilities and capacity for climate stress-testing and address stakeholders’ concerns over the status quo of this field.

Research Keywords

Climate risk, Flooding risk, Coastal asset risk, Multi-hazard models, Loss function, Real estate markets, behaviour biases, Credit risk modelling, Mortgage default, Bank capital, Geospatial modelling, Spatio-temporal climate stress testing, Financial contagion, Macro-economic impact, Multi-criteria decision making