Ceri Dell, Richard Edwards, Anna Gilmore, Lindsay Robertson and Janet Hoek*

Dell C, Edwards R, Gilmore A, Robertson L, Hoek J. Tobacco industry ‘transformation’ – more smoke and mirrors? Public Health Expert Blog. 7 June 2022. https://blogs.otago.ac.nz/pubhealthexpert/tobacco-industry-transformation-more-smoke-and-mirrors/

This blog examines tobacco industry claims that it is ‘transforming’ and the possible implications for public health. We draw extensively on an article examining tobacco industry transformation1 from the Tobacco Control 30th anniversary issue and consider a response from tobacco industry spokespeople.2 Finally, we review tobacco companies’ responses to the Smokefree Aotearoa Action Plan and whether their reactions support claims the tobacco industry is transforming.

Background

In recent years, some tobacco companies have claimed that they are ‘transforming’ and now support public health goals, including reducing smoking prevalence. For example, Philip Morris International (PMI) announced their intention to transform in 2016 and now claim to be building a ‘smoke-free future’, ‘unsmoking’ the world, and helping people who smoke to ‘unsmoke’ (Figure 1).

Similarly, in 2020, British American Tobacco (BAT) announced its new corporate strategy – ‘To Build A Better Tomorrow’ (Figure 2) – by reducing the health impact of their business through ‘Portfolio transformation’ that focuses on new non-combustible, ‘reduced risk’ tobacco and nicotine products. Imperial Brands and Altria have made similar claims.

Figure 1: source https://www.pmi.com/our-transformation/our-interactive-transformation (accessed 13th May 2022)

Figure 2: source https://seekingalpha.com/article/4418669-british-american-tobacco-stock-has-significant-upside-potential (accessed 13th May 2022)

These claims appear welcome changes in direction. However, tobacco industry transformation has to date largely been defined, conceptualized and evaluated by the industry or through the PMI-funded Foundation for a Smokefree World’s Tobacco Transformation Index project. This is highly unsatisfactory given industry-based narratives, research and activities have and continue to prove highly deceptive and cause delays in effective regulatory actions.3 4 Hence, independent and critical assessment of tobacco industry transformation is urgently needed.

The recent publication: “Evaluating tobacco industry ‘transformation’: a proposed rubric and analysis”,1 provides such an assessment. It proposes a definition and outlines criteria for tobacco industry transformation, evaluates whether those criteria are being met, and hence whether meaningful transformation is occurring, and assesses the feasibility of such transformation.

Transformation definition

We defined a transforming tobacco company as one demonstrating substantial, rapid and verifiable progress towards eliminating the production and sale of conventional smoked and oral tobacco products within five years in all markets where the company operates. This timeline allows a reasonable time for transition whilst recognising the urgency of ending the smoking epidemic to protect the health of current and future generations. It also acknowledges the agency that the industry possesses (companies have complete authority over whether and when they end production and sales), and the decades the industry has had to prepare for an end to producing smoked tobacco products since their severe health effects first became clear in the 1960s.

Transformation criteria and evaluation of progress

We proposed four criteria, three essential and one non-essential for gauging industry transformation. Using documentary evidence, analysis of Euromonitor data, and appraisal of the Tobacco Transformation Index report (noting the caveat that this index is wholly funded by PMI through its ‘Foundation for a Smokefree World’ and has been criticised for its lack of independence and flawed methodology) we assessed whether the industry collectively, or any individual tobacco company, meets these criteria. We focused particularly on PMI as the company at the forefront of transformation claims.

Criterion 1 (essential and primary criterion): evidence of substantial progress towards eliminating the production, distribution, marketing and sales of conventional tobacco products within 5 years

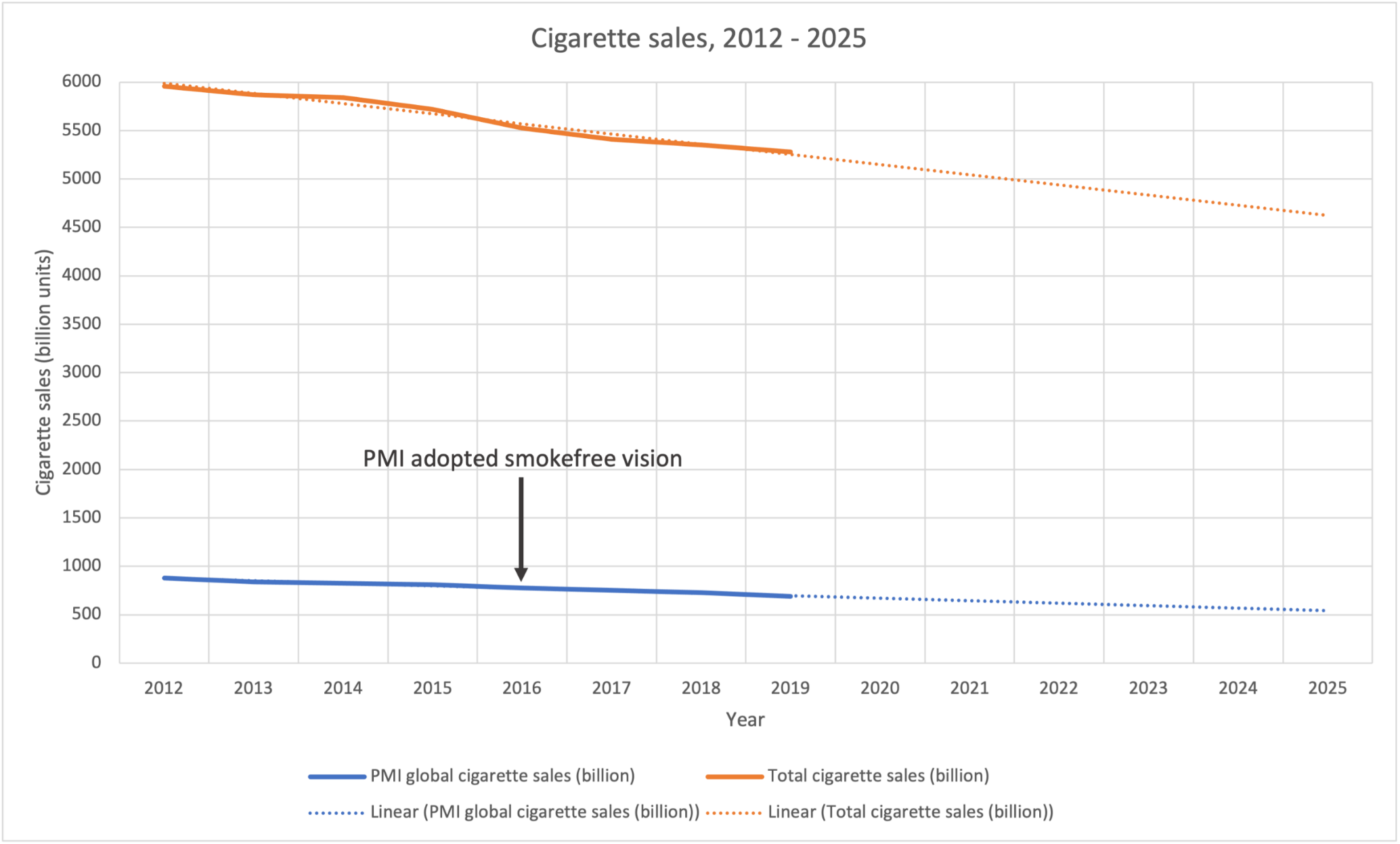

We found no evidence of a rapid decrease in smoked tobacco product sales, or any substantial change in the trajectory of the gradual decline in cigarette sales which has occurred since 2012 (see figure 3). The current trajectory will not come close to eliminating sales within five years.

Figure 3: Global and PMI cigarette sales 2012-19 with linear projection to 2025 (from Euromonitor retail volumes data)5

Criterion 2 (essential): no obstruction of core and innovative tobacco control measures in any jurisdiction

Criterion 3 (essential): evidence of action to reduce uptake and eliminate disparities in use of conventional tobacco products

We found evidence from numerous countries that tobacco companies continue to block tobacco control policies and obstruct efforts to prevent youth uptake and address inequities in smoking prevalence.

Criterion 4 (non-essential): replacement of conventional tobacco products with a portfolio of acceptable alternative products or services

Some tobacco companies have partially met the fourth (non-essential) criterion, through developing portfolios of new nicotine and tobacco products (NNTPs) such as e-cigarettes and vaping products that are likely to be less harmful than smoking if used as complete replacements for conventional cigarettes. However, to be consistent with transformation, new product marketing and deployment need to maximize positive and minimize negative impacts on population health.

For example, NNTPs should replace rather than being additive to combustible tobacco products sales. The continuing slow decline in sales of smoked tobacco products described above and evidence from industry internal strategy documents and investor presentations suggests this is not the case and that NNTPs may result in growth in companies’ overall nicotine and tobacco product production and sales.

A transformative approach would see these alternative products used largely by existing and recently quit adult smokers, with people who smoke and use NNTPs (‘dual-users’) quickly transitioning to exclusive use of NNTPs. However, marketing approaches often target young people resulting in high uptake of vaping products among this age group, and the degree to which dual-users transition completely away from smoking is unclear, with most continuing to smoke at least in the short term.6 7

Transforming companies would focus their product portfolios on the least harmful products and those which are most likely to reduce smoking prevalence. However, PMI’s NNTP portfolio is dominated by heated tobacco products which lack evidence that they aid smoking cessation,8 may be mainly used in addition to smoking,9 10 and which are likely to be more harmful than vaping products.11 12

Feasibility of industry transformation

We investigated the financial viability of transformation and concluded that evolving into companies largely supplying NNTPs to adult current and former smokers is not a sustainable business model. For example, the market for NNTPs if restricted to adult current smokers (the group the tobacco industry claims it exclusively targets with these products) would be highly constrained and would rapidly decrease in size as people who smoke died or stopped smoking and vaping over time. Also, the tobacco industry would likely face fierce competition from non-tobacco industry producers, further reducing their share of a limited and dwindling market.

PMI’s counter-claim

PMI has responded to our paper through a response published on Qeios, a non-peer reviewed commentary site.2 Their response concurs that the core of transformation is the rapid elimination of the production and sale of conventional tobacco products and that a clear roadmap of measures, including ‘phase-out’ policies, is required to accelerate an end to the smoking epidemic. They claim that their transformation programme is progressing rapidly and with urgency, mainly citing evidence relating to our (non-essential) fourth criterion. For example, they argue that NNTPs (largely heated tobacco products for PMI), are a growing source of revenue in an increasing number of markets, and attract a high proportion of R & D expenditure.2

However, their response is unconvincing. Firstly, with regards to the first and core criterion, they argue a reduction in global sales from 847 billion cigarette sticks in 2015 to 625 billion by 2021 – an annual decline of 37 billion sticks per year – represents progress. This rate of decrease would not result in zero sales until around 2038 and will not come close to ending smoked tobacco product sales within five years. Accepting this slow rate of decline and arguing that a five year time period is ‘unrealistic’ seems to contradict PMI’s assertion that it is acting with “urgency” to achieve its smoke-free goal. Further, as figure 3 shows, the decline in PMI’s cigarette sales following the introduction of IQOS in 2015 and the adoption of the smokefree vision in 2016, largely continues pre-existing trends.

The PMI authors also argue that PMI alone stopping the sale of cigarettes would do ‘nothing’ to end smoking; claiming that people who smoke would switch to competitors’ cigarettes.2 This argument shows little confidence in their non-combustible products, which they claim are highly appealing and effective alternatives for people who smoke, and implies they have little faith that these products will “unsmoke” the world or replace smoking. Wouldn’t a company that was aiming to be a leader in ending the smoking epidemic at least try ending sales of their combusted products in some markets and see what happens?

In relation to the second and third essential criteria, PMI’s representatives did not explain PMI’s long history and continuing opposition to tobacco control policies. Nor did they explain why the company continues to launch new brands in lower income countries like Indonesia, or why PMI supplies and markets products such as capsule cigarettes (e.g., ‘Marlboro Mega Ice Blast Menthol’ in New Zealand) that appeal differentially to youth.13 14 Nor did the response address our argument that transformation would not be a financially viable strategy if the company marketed and supplied NNTPs only to people who already smoke, as they claim to aim to do.2

Despite the evidential gaps and logical flaws in PMI’s response, some claims have a superficial appeal. For example, they acknowledge, after decades of opposing almost all regulatory measures, that we need “policies that will lead to people stop wanting to buy cigarettes in the first place” and that “our actions can contribute to reducing demand for cigarettes”. Further, they profess support for “a clear regulatory roadmap agreed by political, regulatory, and public health stakeholders”, and suggest this road map should include ‘phase-out policies’. 2

However, further reading reveals that PMI’s apparent U-turn has strings attached. For example, the response states that they will ‘not oppose’ increased restrictions on combustible tobacco products such as plain packaging and ‘sensibly’ increased taxes. However, such support is conditional on regulators “allow[ing] for availability and differentiation of smoke-free alternatives.” Similarly, it states that PMI will encourage adult smokers, who do not quit, to switch to smoke-free alternatives, but only in “markets where our smoke-free products are available“. A truly transformed company would surely give unequivocal support to effective tobacco control measures and assist people who smoke to quit smoking, regardless of the status of their combustible and non-combustible products in the local market?

The New Zealand Action Plan for Smokefree Aotearoa and tobacco industry transformation

The responses (or in some cases lack of response) of the tobacco companies to the Smokefree Aotearoa 2025 Action Plan provide further evidence about the reality of tobacco industry transformation.

For example, PMI has thus far failed to support (or even comment on) the Action Plan and did not write a submission for the consultation process. Their lack of enthusiastic support for a plan that sets out a comprehensive regulatory roadmap and includes ‘phase-out’ measures like substantial reductions in retail supply and mandated reduction of nicotine, is surprising. More than any other recent regulatory initiative, the Action Plan could ensure that “unsmoking” succeeds in Aotearoa. PMI’s silence stands in contrast to the grandstanding claims made in its Qeios letter. 2

Other ‘transforming’ tobacco companies have failed this test even more comprehensively. For example, BAT, which has around 70% of the market for cigarettes and tobacco in New Zealand, in its submission opposed almost every regulatory measure included in the draft Action Plan15 and was found to be marshalling opposition among retailers.

Conclusions

We found minimal evidence that the tobacco industry is truly transforming. Our assessment rather suggests that some tobacco companies are pursuing a deceptive ‘pseudo-transformation’ strategy that will neither rapidly eliminate of smoked tobacco products nor reduce the enormous harm these products cause. This strategy could enable companies to enhance their credibility and thus their ability to influence policy-makers and obstruct robust and transformative tobacco control policies. This threat underlines how crucial complete and timely implementation of the Smokefree Aotearoa Action Plan is and highlights the need for continued protection of the policy-making process, as required by Article 5.3 of the Framework Convention on Tobacco Control which New Zealand signed in 2003.

The ‘transformation’ narrative, which positions industries that cause public health and societal harms as part of the solution to those problems, is not confined to the tobacco industry.16 In an era where disinformation is pervasive, there is a risk that the tobacco industry and its associates may shape the development, framing and language of ‘transformation’ and its subsequent evaluation. We believe independent public health organisations and practitioners need to lead these debates and ensure robust and independent evaluation of industry transformation. We hope that our paper contributes to that endeavour.

* Author details: Ceri Dell, Richard Edwards, and Janet Hoek are based in the Department of Public Health, University of Otago, Wellington. Lindsay Robertson is based in the Department of Preventive and Social Medicine in the University of Otago, Dunedin. Anna Gilmore is based in the Tobacco Control Research Group at the University of Bath, UK.

* Funding: There was no specific funding supporting the preparation of this blog or the paper ‘Evaluating tobacco industry ‘transformation’: a proposed rubric and analysis.’ None of the authors have received any funding or support from the tobacco industry or affiliated organisations. Anna Gilmore acknowledges the support of Bloomberg Philanthropies’ Stopping Tobacco Organizations and Products funding. Lindsay Robertson is supported by a Royal Marsden Fast-Start grant UOO2028. These funders had no role in the study design, data collection and analysis, decision to publish or preparation of the blog or the paper.

References

- Edwards R, Hoek J, Karreman N, et al. Evaluating tobacco industry ‘transformation’: a proposed rubric and analysis. Tob Control 2022;31(2):313-21. doi: 10.1136/tobaccocontrol-2021-056687 [published Online First: 2022/03/05]

- Gilchrist M, Motles J. Review of: Evaluating tobacco industry ‘transformation’: a proposed rubric and analysis: Qeios; March 22 2022 [Available from: https://www.qeios.com/read/WMWXQ6 accessed May25 2022].

- Briggs J, Vallone D. The Tobacco Industry’s Renewed Assault on Science: A Call for a United Public Health Response. Am J Public Health 2022;112(3):388-90. doi: 10.2105/AJPH.2021.306683

- Cummings KM, Morley CP, Hyland A. Failed promises of the cigarette industry and its effect on consumer misperceptions about the health risks of smoking. Tob Control 2002;11:i110–i17.

- Euromonitor Passport. Global retail volume 2021 [Available from: https://go.euromonitor.com/passport.html, accessed 24th Feb 2021].

- Miller CR, Smith DM, Goniewicz ML. Changes in Nicotine Product Use among Dual Users of Tobacco and Electronic Cigarettes: Findings from the Population Assessment of Tobacco and Health (PATH) Study, 2013-2015. Subst Use Misuse 2020;55(6):909-13. doi: 10.1080/10826084.2019.1710211 [published Online First: 2020/01/18]

- Schwamm E, Noubary F, Rigotti NA, et al. Longitudinal Transitions in Initiation, Cessation, and Relapse of Smoking and E-Cigarette Use Among US Youth and Adults: medRxiv (preprint); August 3 2021 [Available from: https://www.medrxiv.org/content/10.1101/2021.08.01.21261431v1 accessed May 25 2022].

- Tattan-Birch H, Hartmann-Boyce J, Kock L, et al. Heated tobacco products for smoking cessation and reducing smoking prevalence. Cochrane Database Syst Rev 2022:Art. No.: CD013790. doi: DOI: 10.1002/14651858.CD013790.pub2.

- Sugiyama T, Tabuchi T. Use of Multiple Tobacco and Tobacco-Like Products Including Heated Tobacco and E-Cigarettes in Japan: A Cross-Sectional Assessment of the 2017 JASTIS Study. Int J Environ Res Public Health 2020;17(6) doi: 10.3390/ijerph17062161 [published Online First: 2020/03/28]

- Sutanto E, Miller C, Smith DM, et al. Concurrent Daily and Non-Daily Use of Heated Tobacco Products with Combustible Cigarettes: Findings from the 2018 ITC Japan Survey. Int J Environ Res Public Health 2020;17(6) doi: 10.3390/ijerph17062098 [published Online First: 2020/04/03]

- McNeil A, Brose LS, Calder R, et al. Evidence review of e-cigarettes and heated tobacco products 2018. A report commissioned by Public Health England. London: Public Health England 2018.

- World Health Organization. Heated tobacco products: a brief. Geneva: World Health Organization 2020.

- Kyriakos CN, Zatonski MZ, Filippidis FT. Flavour capsule cigarette use and perceptions: a systematic review. Tob Control 2021 doi: 10.1136/tobaccocontrol-2021-056837 [published Online First: 2021/10/06]

- Hoek J, Gendall P, Eckert C, et al. Young adult susceptible non-smokers’ and smokers’ responses to capsule cigarettes. Tob Control 2019;28(5):498-505. doi: 10.1136/tobaccocontrol-2018-054470 [published Online First: 2018/10/05]

- Robertson L. Tobacco industry responses and arguments in response to the proposed action plan for New Zealand’s Smokefree 2025 goal. Presented in Symposium 3 The Action Plan for New Zealand’s Smokefree 2025 goal: a blueprint for the smoking endgame? Society for Research on Nicotine and Tobacco. Baltimore, Maryland, USA, March 15-18, 2022.

- Li M, Trencher G, Asuka J. The clean energy claims of BP, Chevron, ExxonMobil and Shell: A mismatch between discourse, actions and investments. PLoS ONE 2022;17(2):e0263596. doi: 10.1371/journal.pone.0263596 [published Online First: 2022/02/17]

Nice summary. The key issue here is substitutes – in this case the TI being able to substitute selling NNTPs for tobacco. And here the role of Governments and global coalitions to set the rules (not the TI) is critical.

I think most people agree NZ has been too liberal with access to NNTPs (e.g. youth vaping, especially by youth who were never smokers). And many would agree/argue that countries on the other end of the spectrum (e.g. Australia) have not made access to NNTPs for smokers wanting to quit as easy as it should be. Governments will need to regulate this transition off tobacco and – for some – through NNTPs to eventual quitting. Whilst the medium term endgame is no tobacco, a long term horizon of low NNTP use is also imperative.

Thus, TI revenue will inevitably decrease. They will not make a transition to NNTPs with an end-date (or tight restrictions) voluntarily. It is up to Governments to set these boundaries that mean the only viable model for the TI to downsize (not maintain volume of sales and revenue) is to completely move out of tobacco and into a more tightly regulated and lower volume NNTP world. And that world will have non-TI competitors selling nicotine.

Regards, Tony Blakely

Thanks for these comments Tony.

I agree robust Govt policies to hasten the end of smoked tobacco products are key (as our analysis suggests that the industry will not do this themselves – whatever they might claim). Given that means declining revenues/profits for the tobacco industry, that mean that managing the regulation of alternative products is very important to get the right balance between making these products available as harm reduced substitutes for people who smoke and can’t or don’t want to quit using nicotine, whilst also minimising the growth in use among young people (as the tobacco industry is clearly incentivised to maximise the size of this market).

One other point though, the tobacco industry could as well/instead transition to providing completely different (hopefully non-harmful, non-addictive) products or service provision – it doesn’t have to stay only in the nicotine products market. Companies can reinvent themselves.

However, there is not much sign of that happening yet, but maybe some of PMI’s moves to buy pharmaceutical-oriented businesses represents this sort of approach. That could be a good thing, but only if it occurs in parallel with a meaningful effort to rapidly eliminate the production and sale of smoked tobacco products, which as our paper demonstrates, so far there is not.

Parking links to my 2019 interaction with PMI’s Moira Gilchrist for those wanting extra material on this topic.

1. 10 questions for Philip Morris on their “transformation”. WordPress 21 Feb, 2019 https://simonchapman6.com/2019/02/21/10-questions-for-philip-morris-international-on-their-transformation/

2. At Philip Morris International, it’s business. As usual. WordPress 26, Mar 2019. https://simonchapman6.com/2019/03/26/at-philip-morris-international-its-business-as-usual/

3. https://simonchapman6.com/2019/02/12/if-we-stopped-selling-cigarettes-tomorrow-someone-else-would-take-our-place/ https://simonchapman6.com/2019/02/12/if-we-stopped-selling-cigarettes-tomorrow-someone-else-would-take-our-place/

The co-opting of retailers as a front group for big tobacco is clearly an international trend. They did this in Tasmania to campaign against our proposals for phasing out tobacco sales, as NZ has done. The tobacco industry name is mud. Nobody trusts them. So they cannot make submissions or issue media releases, and having no credibility means they can only use front groups. Also the retail organisations embed themselves into political parties and make donations. So the tobacco industry funnels money through these peak retailer organisations .